")

")

for transfer pricing safety

for transfer pricing safety

In order to prepare a benchmarking study that meets the client’s demands there are certain factors that must be considered:

- correct understanding of the functional profile and risks of each entity participating in the transaction as well as the market context in which they operate;

- detailed research of databases used for selecting and analyzing the independent companies that meet the criteria of comparability;

- determining and making the necessary adjustments regarding the comparability;

- interpretation and use of collected data as well as determination of market value.

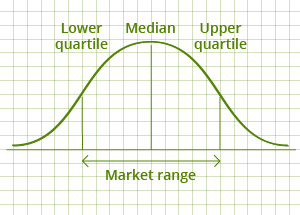

The right answer to the question "how much does a benchmarking study cost?" - we are talking here about a market where quality standards are taken into account and the used databases are approved - is that the arm's length range is the EUR 2,500 median.

If you do not feel prepared at the moment to conduct a customized benchmarking study for your company, but you would like to find out the profit margins by industry / by type of transactions, please go to the "Benchmarking studies library" section. For a customized benchmarking study please go to one of the "I need a benchmarking study" section, depending on the type of business.

If the business operations are not fully analyzed, you can draw up your own benchamarking study based on data provided by www.studiidebenchmarking.ro.