This section includes a list of the most frequently asked questions on benchmarking studies.

1. What are benchmarking studies?

Benchmarking studies are a critical part of any transfer pricing documentation file or policy and are mainly used to:

- test the arm's length nature of the related party transactions in preparing a transfer pricing documentation file;

- set the mark-up attached to the transactions carried out between related parties as part of tax planning exercises;

- determine the arm's length range deemed to provide an estimate of an arm's length price.

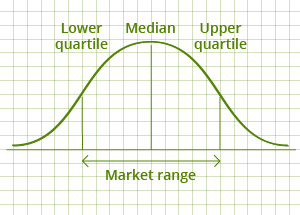

The purpose of benchmarking studies is to determine the general conditions surrounding the transactions conducted by third parties on a given market. Such studies help elicit a range of values, i.e. the so-called arm's length range or mark-up range. Statistically, arm's length range is defined by the lower quartile and upper quartile and is the range of values of price or profit attached to the comparable transactions between comparable unrelated parties.

Where a transfer price determined by a taxpayer for a transaction under review (or the profitability derived by taxpayer from such transaction) is not to be found in the applicable arm's length range, the competent tax authority will determine the arm's length price of the transaction under review using the median value of that arm's length range.

Example: Suppose that company A provides software development services for a related party and derives a 3% mark-up on top of its operating expenses in relation to such services. In order to test the arm's length nature of the transaction (i.e. provision of software development services), a benchmarking study was prepared showing that arm's length range for software development services falls within 4% and 8% with a median at 6%. As company A derives a 3% profitability under the lower quartile (i.e. 4%) and supposing that there are no other business considerations to account for such profitability, the competent tax authority becomes entitled to adjust the applicable transfer prices at the median level (i.e. 6%).

2. What databases are most often used to prepare benchmarking studies?

According to the specifics of the transaction under review and consequently the type of data required to conduct a benchmarking study, the most frequently used databases are as follows:

- Amadeus – contains information on more than 3 million companies (except financial companies such as banks) from 41 European countries, including all member states of the European Union;

- ORBIS (also including the data contained in the Amadeus database) – contains both information on financial companies and information on companies in all industries operating globally, therefore not being limited to the European area;

- Royaltystat – is an on-line available database containing information on more than 15,000 license agreements for intellectual property rights;

- LoanConnector – is a database compiled by Thomson Reuters containing information on more 220,000 financial transactions involving loans or securities;

- Bloomberg – similar to LoanConnector, is a database containing information on financial transaction involving loans and various types of securities.

In investigating transfer prices, Serbian tax authorities will probably use the Amadeus/Orbis databases.

3. How often benchmarking studies must be updated?

In general benchmarking studies should be updated on an annual basis to reassess the impact of the prevailing market conditions on companies’ profitability. Nevertheless, where a company operates on a steady market and its results do not vary significantly from year to year, benchmarking studies can be reasonably updated every two years.

4. What are the steps in preparing a benchmarking study?

The main steps in preparing a benchmarking study are as follows:

- electronic identification: This step involves the designing a search strategy suitable for the transaction under review in order to identify an initial sample of comparables in the database used for the study;

- quantitative screening: This step involves a selection of the comparables in the initial sample according to specific quantitative criteria (if possible) in order to ensure on the one hand that the comparability degrees of the remaining comparables is increased and on the other hand that the resulting sample is reduced to a size that is easier to manage in the following steps;

- qualitative screening: This step involves an assessment of the remaining comparables according to qualitative characteristics in order to ensure that the final sample only contains results that are reasonably comparable to the transaction under review;

- determination of results: Once the final sample of comparables has been obtained, for each of them a specific selected indicator (if no such selected indicator was already available) is determined according to the particular type of the tested transaction and the required arm's length range is then determined based on such results.

5. How much does it cost to prepare a benchmarking study?

According to the complexity of the wanted benchmarking study, the type of database that must be used and the workload involved, the price for a detailed benchmarking study may vary between EUR 1,000 and EUR 10,000.

6. Are benchmarking studies conducted at the EU level acceptable to the Serbian tax authorities?

According to Transfer Pricing Rulebook, benchmarking studies must be first prepared locally (i.e. in Republic of Serbia). If no sufficient comparable can be identified locally, the search can be extended to the other countries in the region that have similar business conditions to those in Serbia.

Nevertheless, even though the Transfer Pricing Rulebook does not specifically mention the next steps in case no sufficient comparables can be identified in the region, the search criteria can be extended to the EU level.

In conclusion, a benchmarking study conducted at the EU level may be used for local purposes as long as unavailability of sufficient comparables at local and regional level can be proven and also provided that the relevant benchmarking study meets the requirements of the Serbian transfer pricing legislation (e.g. requirement on a company’s status of independence).

7. Can benchmarking studies prepared at group level be also used for local purposes?

Generally, benchmarking studies prepared at the group level could be used as a starting point in preparing studies for local purposes. However, the practice shows that the search strategies employed at group level frequently fail to fully meet the requirements of the local legislation (i.e. particularly the requirement to test comparability locally at first or the company’s status of independence).

8. What are the most frequent errors in preparing a benchmarking study?

Most often the reliability of a benchmarking study is affected by either a failure to adjust the search strategy to both the specific requirements of the local legislation and the principles of the OCED Guidelines, or a failure to adjust such search strategy to the particularities of the type of data available in each individual database.

Also, it is crucial that benchmarking studies be auditable and replicable when inspected by the competent tax authority. This involves that the company that prepared the benchmarking study is able to prove itself as legitimate owner of the database that was used in preparing that study. As databases are updated on an annual basis, where transfer prices are investigated after a given time since the preparation date of the transfer pricing documentation file / benchmarking study, it may be necessary during a tax inspection for the company that prepared the report to provide the competent tax authority with the version of the database that was used in preparing the study. This is precisely required to prove that the competent tax authority would obtain the same results as the party preparing the study if it applied the same search strategy in relation to that database in conducting the relevant benchmarking study.

")

")

for transfer pricing safety

for transfer pricing safety